How Electric Arc Furnaces (EAF) are Reshaping Scrap Steel Demand

Electric Arc Furnaces are fueling a scrap steel gold rush as steel decarbonizes. Discover how circular steelmaking reshapes markets, geopolitics, and the $1.5T green steel race. Who will own the net-zero era?

SUSTAINABLE METALS & RECYCLING INNOVATIONS

As the global steel industry races toward sustainability, one key innovation is transforming the production landscape: Electric Arc Furnaces (EAFs). With a focus on decarbonization, circular steelmaking, and evolving raw material demand, EAF technology is rapidly changing how we think about steel — and more importantly, the market dynamics of scrap steel.

In this in-depth market analysis, we’ll break down how the widespread adoption of EAFs is driving a paradigm shift in scrap steel demand, impacting global supply chains, pricing models, and environmental strategies.

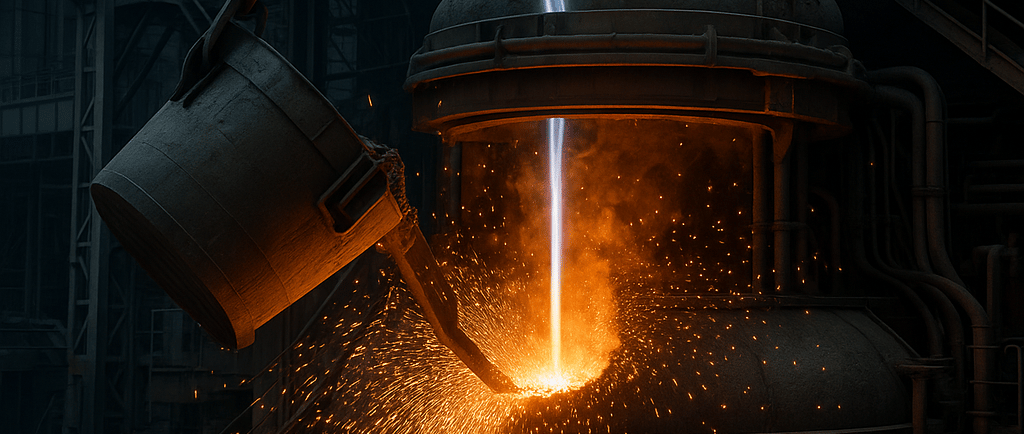

What Is EAF Technology and Why Is It Transforming the Steel Industry?

For decades, traditional steelmaking relied heavily on blast furnace-basic oxygen furnace (BF-BOF) methods, which primarily use iron ore and coking coal. While robust and scalable, the BF-BOF process is also extremely carbon-intensive — emitting over 2 tons of CO₂ for every ton of steel produced. In a world confronting climate risks, this emission profile is increasingly untenable.

Electric Arc Furnace (EAF) technology offers a more sustainable and energy-efficient alternative. EAFs use high-current electric arcs to melt metallic feedstock — predominantly scrap steel — drastically reducing carbon emissions. Compared to the BF-BOF route, EAFs can slash CO₂ emissions by up to 75%, especially when powered by renewable electricity.

This game-changing shift isn't just about lower emissions. EAFs offer greater operational flexibility, faster start-up times, and reduced capital investment costs. These attributes make EAFs well-suited for modular, decentralized production models — fitting neatly into future-ready urban steel ecosystems.

Additionally, EAFs support product innovation, including high-strength, high-performance steels, especially when integrated with smart scrap sorting, AI-driven feedstock analysis, and automation platforms. This ability to innovate materials while remaining low-carbon is positioning EAFs at the forefront of next-generation manufacturing.

This shift aligns seamlessly with global decarbonization goals and ESG principles, positioning EAFs as focal points in the clean energy transition for heavy manufacturing industries.

The Global Rise of EAF Technology and Its Strategic Implications

Growing EAF Capacity Worldwide

Globally, steel producers are ramping up investments in EAF facilities. According to the World Steel Association, EAF-based crude steel production currently represents about 30% of worldwide output, with this figure projected to reach 50% by 2050 under the agency’s Sustainable Development Scenario. In some markets, growth is happening even faster.

- United States: The U.S. is a mature EAF market, with over 70% of steel made via electric arc routes. Giants like Nucor and Steel Dynamics are leading in EAF innovation and vertical integration, often sourcing and processing scrap in-house.

- China: Historically reliant on BF-BOF, China is now embracing EAFs to meet its 2060 carbon neutrality goal. By 2025, China's EAF capacity is expected to exceed 200 million tonnes, with a clear emphasis on upgrading legacy infrastructure for clean production.

- India and the Middle East: These regions are combining EAFs with direct reduced iron (DRI) and natural gas-based feedstocks, leveraging access to low-cost energy to facilitate green steel production.

- Europe: Steelmakers like ArcelorMittal, SSAB, and Voestalpine are investing heavily in hybrid EAF-DRI facilities, representing a shift toward net-zero infrastructure across the continent.

Policy-Driven Growth

Policy frameworks are accelerating this transformation:

- European Union Green Deal mandates deep cuts in industrial emissions, incentivizing EAF-scale decarbonization.

- The U.S. Inflation Reduction Act allocates billions for clean energy transition, with explicit incentives for green manufacturing, including EAF steel.

- Carbon Border Adjustment Mechanisms (CBAM) are reshaping global competitiveness by linking emissions intensity directly to import/export economics — encouraging low-carbon exports and penalizing carbon-heavy processes.

These policy levers are creating a regulatory moat for firms adopting EAFs early. Additionally, pressure from institutional investors demanding robust ESG compliance under frameworks like the TCFD (Task Force on Climate-Related Financial Disclosures) and Sustainability Accounting Standards Board (SASB) is further amplifying the push toward EAF technologies.

How EAFs Are Driving an Evolution in Scrap Steel Demand

At the heart of EAF-based steelmaking lies a crucial input: scrap steel. Its significance is rising exponentially as manufacturers seek lower-carbon inputs that enable circularity without compromising material integrity.

A Structural Shift in Raw Material Requirements

Traditional BF-BOF methods rely on mined inputs such as iron ore and metallurgical coal. These processes not only have immense carbon footprints but are also subject to geopolitical tension and price fluctuations.

In contrast, EAFs prioritize ferrous scrap — recycled steel from end-of-life vehicles, appliances, industrial waste, and obsolete infrastructure. This pivot has triggered a structural rebalancing:

- Increased per-ton scrap consumption: EAFs commonly run on 90-100% scrap steel. Given global steel production exceeds 1.8 billion metric tons annually, even a 10% shift to scrap dependence could translate into over 180 million additional tons of scrap required per year.

- Broad grade range integration: From heavy melting scrap (HMS) to shredded and bundled light scrap, EAFs adapt to multiple input forms, increasing circular economy uptake and minimizing landfill use.

- Localized value chains: Since scrap steel is bulky and often degrades in transit, production supply chains are becoming regionally anchored, strengthening local economies and insulating producers from international freight cost volatility.

This marks a pivotal realignment in the global steel industry from a linear, extractive model toward a circular, materials recovery-driven approach.

Demand-Driven Price Volatility

As EAF capacity increases, the link between scrap steel pricing and EAF utilization rates grows tighter. Unlike iron ore, which has futures markets and relatively predictable demand, scrap markets remain fragmented, localized, and often informal.

- Data from Fastmarkets shows that U.S. benchmark shredded scrap prices have ranged between $250-$700 per ton over the last five years, with sharp spikes corresponding to EAF commissioning and infrastructure stimulus programs.

- Global supply-demand imbalances, particularly during post-COVID infrastructure booms, further exacerbated volatility in the scrap market.

- Substitute feedstocks like hot briquetted iron (HBI) and pig iron prices are also fluctuating, often tracking scrap shortages in premium grades.

Producers increasingly require insight-driven procurement tools, scrap quality analytics, and long-term supplier relationships to hedge against raw material risk and secure just-in-time delivery frameworks.

Quality and Purity Challenges

Not all scrap is created equal. For flat-rolled steel, automotive-grade materials, or high-tensile structural products, strict chemical composition and low contamination levels are non-negotiable.

- Residual Elements (Copper, Tin, etc.): If not adequately removed, these “tramp” metals can compromise mechanical properties and product weldability.

- As a result, premium feedstocks like direct reduced iron (DRI) and hot briquetted iron (HBI) are increasingly used to supplement the scrap stream and dilute impurities.

- An evolving ecosystem of optical AI sorting systems, eddy current separators, and low-magnetic field pulsing systems is enabling better segregation and reuse of high-quality scrap.

Companies like Boston Metal and Electra are exploring electrowinning and direct electrolysis methods to refine or supplement scrap steel inputs, unlocking a potential frontier for ultra-pure feedstocks that bypass gas-based reduction entirely.

Scrap Steel’s Decarbonization Revolution – Where Circular Dreams Meet Market Realities

The rise of Electric Arc Furnaces (EAFs) isn’t just changing how we make steel—it’s rewriting the rules of resource economics. At the heart of this transformation? Scrap steel, once relegated to junkyards, now sits center stage as industrial gold. Let’s unpack how this shift is accelerating circularity, reshaping global trade, and creating winners in the race to net-zero.

Circular Steelmaking: More Than Recycling—It’s a Climate Weapon

Picture this: For every ton of steel recycled in an EAF powered by renewables, up to 97% of CO₂ emissions vanish compared to traditional blast furnaces. That’s not incremental progress—it’s a quantum leap.

How? EAFs thrive on scrap’s near-infinite recyclability. Steel retains its strength forever, and today’s scrapped car could be tomorrow’s skyscraper beam. But the magic isn’t just in reuse:

Water and waste? Turned into assets: Modern EAF plants recycle 90% of process water and transform slag into cement or roads.

Quality hurdles? Tech is cracking the code: AI sorters now zap copper and tin contaminants from scrap piles, while blending in 5–20% premium DRI/HBI creates virgin-quality steel.

The bottom line: Circular steel isn’t eco-friendly PR—it’s a $1.5 trillion decarbonization engine.

Scrap’s Geopolitical Chessboard: Who Wins, Who Scrambles?

Not all nations enter the EAF era equally. Scrap availability and policy agility are dividing the field:

China’s Scrap Surge: With 90% of steel still made in carbon-spewing blast furnaces, China’s sprint toward 200+ million tons of EAF capacity by 2025 is staggering. By 2050, this could cut 657 million tons of CO₂ yearly—equal to silencing Germany’s entire carbon footprint. But there’s a catch: Rampant construction waste won’t cover demand. Scrap imports loom.

India’s Import Addiction: EAFs will drive 50% of India’s steel output by 2030 (up from 15%). But domestic scrap meets only half of the coming 65 million-ton demand. Result? A 20–30 million ton import gap—turbocharging markets from Turkey to Australia. Zero import duties and GST reforms are fast-tracking this hunger.

Europe’s Double Bind: CBAM tariffs and EU Green Deal rules make scrap precious. Yet volatile demand (consumption fell 8% in 2022) and energy costs threaten momentum. Abundant high-quality scrap is Europe’s ace—but only if renewables keep EAFs humming.

2030 Forecasts: The Scrap Crunch Is Coming

Brace for a scrap market on fire:

Global demand will rocket past 800 million tons by 2030 (up from 650M today).

Trade wars will flare as export bans (like EU rules blocking scrap to non-OECD nations) collide with import desperation in India and Southeast Asia.

Overcapacity warning: 165 million tons of new global steel capacity by 2027 could crash utilization to 70%, squeezing green investments exactly when they’re needed most.

The decarbonization pathways are clear, but rocky:

1. EAF-DRI Hybrids: Green hydrogen-DRI will plug scrap gaps in sun-rich hubs (think Oman or Australia).

2. Carbon Capture’s Last Stand: 74% of blast furnaces are exploring CCUS, but $100+/ton costs make it a bridge, not a destination.

3. Hydrogen’s Long Game: Projects like HYBRIT promise zero-emission steel—if H₂ infrastructure scales fast.

Who Needs to Act—and How

→ Policymakers:

Tax carbon like it’s toxic: $15–50/ton fees make EAFs unbeatable (China’s ETS proves it works).

Turn scrap informal → industrial: Fund collection networks and tax breaks for processors (India’s GST overhaul is a model).

Electrify everything: Decarbonize grids now—EAFs are only as clean as their power source.

→ Steel Producers:

Lock down scrap like it’s Bitcoin: Forge long-term deals with recyclers or build DRI plants near cheap energy.

Quality = survival: Deploy AI sorters to upgrade obsolete scrap into “premium feedstock.”

Marry renewables: Partner directly with wind/solar farms (like Nucor’s Texas wind deal).

→ Investors:

Bet on green steel hubs: Back integrated DRI-EAF facilities where sun and wind are cheap (Chile, Australia, Nevada).

Dominate scrap logistics: Port infrastructure and containerized shipping are hidden gems.

Fund the unsexy tech: Hydrogen electrolysis and CCUS need capital to cross the valley of death.

The Verdict: Scrap Isn’t Waste—It’s the New Oil

The data screams urgency: Regions rich in scrap and renewables (U.S., EU) will dominate low-cost green steel. Coal-heavy giants (China, India) face brutal—but necessary—transitions. By 2030, scrap will morph from commodity to strategic decarbonization oxygen, making today’s investments in circular infrastructure non-negotiable.

"The future of steel is electric, circular, and hyper-regional. Those who control the scrap value chain won’t just adapt to the net-zero era—they’ll own it."

What’s your move?

Connect

Your trusted partner for scrap metal procurement.

CONTACT

About

haroon@tdcventures.com

+1-307-655-7593

© 2025. All rights reserved.

NEWSLETTER